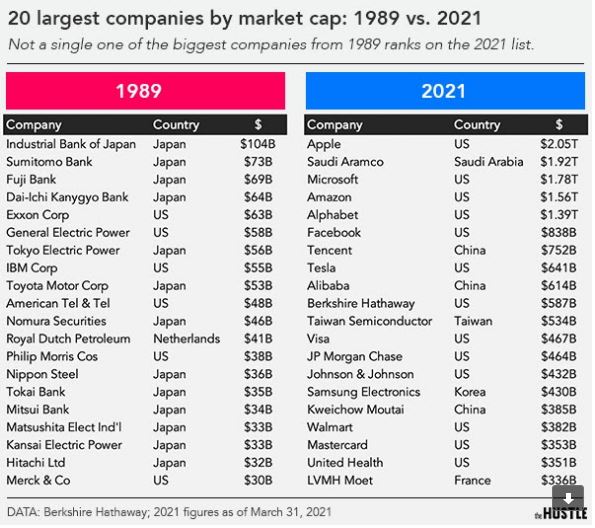

This is in interesting graphic. In 1989, the largest corporations in the world included a whole bunch of banks, a few oil companies, and several big capital heavy industries like General Electric. In only one third of a century, EVERY ONE of the top 20 from 1989 had fallen off the list. Also note that 13 of the top 20 from 1989 were Japanese companies and exactly none of them were from Japan in 2021.

Note as well the incredible inflationary spiral of asset values in the totals. In 1989, the top company by market capitalization, Industrial Bank of Japan, was $104 billion, but in 2021, the bottom of the top 20, LVMH Moet, was at $336 billion.

(If you are like me and don’t know what LVMH Moet is: “LVMH Moët Hennessy Louis Vuitton, commonly known as LVMH, is a French holding multinational corporation and conglomerate specializing in luxury goods, headquartered in Paris.”)

If we take this chart at face value, and assume that market capitalization is a valid and comparable way to evaluate industries over time, this chart tells an an incredible tale of accelerated business change within a single career lifetime. The companies at the top of the international hierarchy all fell, and they fell mostly from one country that was well known for having a highly educated workforce and a stable business environment. Whatever caused the Japanese to fall behind, it wasn’t war or pestilence.

The first thing that strikes me is the incredible value software and software enabled device has brought to the world. Apple does not make food, clothing, or shelter, but it makes something the world wants very badly. They want to see information served by Google and Facebook, and they want to buy stuff on Amazon, all companies at the top (Alphabet is Google). Note that Tencent and Alibaba are the Chinese equivalent of the US tech giants. If you take out the tech companies, you’re left with one oil company, some drugs, finance, and a little retail. But mostly, there is tech.

An interesting coincidence is that 1989 was the year of Tiananmen Square in China, and the fall of the Berlin Wall in Europe. The political and regulatory environment we have now was settling in to place then. Neither Apple nor Wal-Mart would be on the list from 2021 but for Chinese low-cost labor, which has been aided by the Chinese state. Tencent and Alibaba may not exist at all if they had to compete with the US tech giants, but the same Chinese state has placed limits on the internet in China and allowed its incumbents to thrive. Much of the massive turnover was driven by China, which replaced Japan as Asia’s manufacturing powerhouse.

So, what happened to Japan and the Japanese industrial output? Did they just get lazy and hand the leadership baton to the more energetic Chinese? This seems unlikely, and perhaps the opposite problem explains the fall.

The Japanese have a word for being overworked at the office and dying suddenly: it’s called karoshi. I recall hearing about this back when Japan, and not China, was the source of US hand wringing about foreign competition. Japanese workers, mostly men, would die at their desks after putting in the expected 70 hour work weeks. To the degree that they took breaks, it was often to bars where they would be expected to get drunk with their co-workers, and under the influence of alcohol, they could speak honestly about issues that couldn’t be discussed in the strict and hierarchical workplace. And then, they would die early, at their desks, in their fifties.

Through this period, the Japanese fertility rate fell, and the percentage of government debt to total output rose. In 1959, the Japanese fertility rate was at 2.1, the rate at which the population is stable, but by 2003, it had dropped to 1.2. In a similar time frame, the percentage of public debt relative to the overall economy rose to 125% in 2003 and stands at 200% now.

In summary, the Japanese engineered a stunning rise from the ashes of World War 2, and then they worked and borrowed themselves right out of the top slots. Perhaps those men should have gone home early to their growing families. Who is going to pay all of that public debt now?

The peak of Japanese output came at the end of the industrial period of manufactured things. In the 1990s, I worked for Sony, a well-regarded Japanese manufacturer of cool gadgets and devices, and yet, Apple is on top now. The top brands from that period, Sony, JVC, Panasonic, are mostly meaningless now. No one wants my old Walkman, not even me. In business, timing holds the dominate hand.

Software is the dominate value add in the world today. We still need oil, and we still need labor, we still need things, but software accelerates and is the force multiplier of the world of things. This process is likely to continue and possibly accelerate further and faster.

Note as well the fall of banks from the 1989 to the 2021 list. Finance companies have taken their place. JP Morgan is not just a retail bank that lends to those who build factories; it’s a finance powerhouse. Visa and MasterCard facilitate transactions on Amazon and Tencent around the world. Money is already digital and fungible and it is about to become more so.

Who will be in the top 20 in 2053, some 32 years on? There is no way to know because innovation and culture moves at a pace that can’t be predicted. I recall reading nothing on the impending fall of the Japanese in 1989 or the decade to follow.

There are, however, a few notable trends. First, it’s well known that the demographics of China are following the Japanese. Nearly everywhere on earth is predicted to have falling populations by 2053. Only Africa has rising populations and so African countries may become the cheap labor force of the future. Might there be African business titans on the 2053 list?

Debt is piled high everywhere including the United States which gets to the inflationary trend so apparent in the graph. The #1 company in 1989 was worth $104 billion and the #1 company in 2021 was worth 20X as much at $2 trillion in 32 years. That’s kind of rise is not just value; that is inflation. Which countries can manage their debts in a declining population trend will be interesting to see.

And finally, there is the issue of more and better technology. Money is being remade by technology and incurring inflationary debt might be a lot harder in the next 32 years. In a perfect world, blockchain technology would remake the regulatory state and business practices so that prices and payments reflect value. It may be here that China makes a mistake and refuses to embrace a cutting edge technology. They regulated the internet in a way that protected their state interests but didn’t prevent the rise of Alibaba and Tencent. Can they do that with Bitcoin, cryptocurrencies, and the world of decentralized ledger technology? They certainly think so, but then, they got away with a lot of things because so many enterprises the world over wanted access to their massive population and allowed them to play by different rules. Now, that population is no longer growing. China of 2053 will not be China of 2021, and everyone knows it.

By 2053, market capitalization might not even be a common metric for establishing value so perhaps we’ve reached the end of these kinds of comparisons. The pandemic years have shown for all what uncertainties can upend markets. Still, superior technology always adds value and the businesses that have it and use it tend to win.